The Guide to

SaaS Metrics

The Guide to

SaaS Metrics

Table of Contents

- Introduction

- Metrics to Measure

- Operationalizing Metrics

- Visualizing Metrics

- Sharing Metrics with Your Board

- Fundraising with Metrics

- Good Luck Out There

- Appendix

Find the levers to grow faster →

GTM analytics that shows you what's working — and what's not.

LTV:CAC

- By

-

Bobby Pinero

Bobby Pinero

Bobby Pinero

Bobby Pinero

15+ years of corporate finance experience, currently co-founder at Equals and board member at Intercom.

What is LTV:CAC?

LTV:CAC is a widely used test of a business’s viability. It compares the lifetime value of a customer to the cost of acquiring that customer. Conceptually, this measures the Return on Investment (ROI) of each dollar spent on customer acquisition.

High vs. Low LTV:CAC

A high LTV:CAC ratio indicates that the customers you bring in are worth more than what it takes to acquire them, and you can safely invest in scaling without an exponential increase in acquisition spend.

By contrast, a low LTV:CAC ratio is a warning sign that your business model may not be sustainable. It signals you’re spending too much to acquire customers relative to the value they provide to the business, which limits growth and inevitably leads to cash flow problems. And we know cash is king.

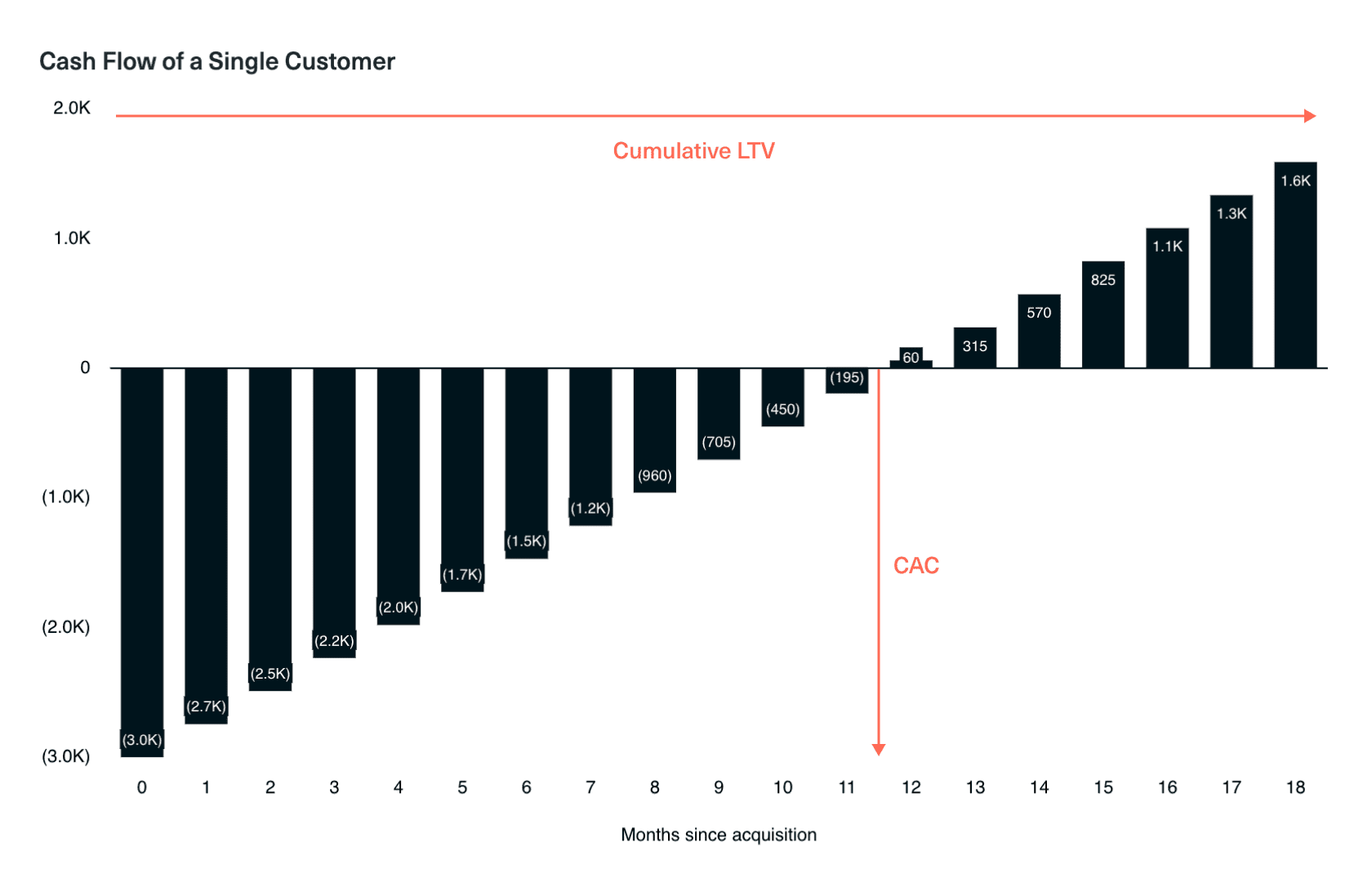

Why use CAC to assess profitability? Because CAC is the primary expense associated with operating a SaaS business. As the business matures, R&D expenses tend to stabilize and are spread across an ever-growing customer base. By contrast, a traditional business like an automaker incurs production costs for every new unit sold.

This dynamic leads to the Triangle of Despair in SaaS. The depth of the triangle corresponds largely to the magnitude of your CAC, while LTV represents the sum of every bar (or the sum of value realized across every period in the customer lifetime). To grow, SaaS companies must minimize CAC while maximizing LTV.

It’s also why SaaS businesses are not valued on earnings (EBITDA). Earnings are a snapshot in time and do not indicate the business’s profit potential. Instead, investors tend to use revenue multiples — which, turns out, can be derived from LTV:CAC — to value a SaaS business.

How to calculate LTV:CAC

As the name suggests, the formula used to calculate LTV:CAC is simply LTV divided by CAC:

It’s good practice to segment your LTV:CAC to reveal underlying dynamics within your customer base that may be masked at the top level. This allows you to optimize against LTV:CAC by doubling down on the acquisition, retention and expansion of your high-LTV:CAC segments, shifting the composition of your customer base and your aggregate LTV:CAC over time.

How to optimize LTV:CAC

Below are the general guidelines for what’s considered a “good” LTV:CAC ratio for an early-stage SaaS business. The highest-performing businesses tend to have an LTV:CAC of greater than three, meaning that for every dollar invested in acquiring a customer, roughly three dollars are returned to the business.

| LTV:CAC | Description |

|---|---|

| 1.0 or below | Unsustainable. The cost to acquire a customer is equal to or less than the value they bring, implying the business is not profitable after accounting for operational costs. |

| 1.0 to 3.0 | Acceptable for growth-stage startups investing heavily in growth. However, the business should aim to improve acquisition efficiency over the long-term. |

| 3.0 | Great. The business is likely generating a good return on investment from its acquisition efforts, after accounting for operational costs. |

| 3.0 to 5.0 (or higher) | Exceptional. However, the business may be under-investing in marketing and could potentially achieve higher growth by scaling acquisition spend. |

To optimize for LTV:CAC, you’ll need to maximize LTV and minimize CAC without negatively impacting retention (and, by extension, reducing LTV to the point where it offsets your CAC savings).

Before continuing, a word of caution. While LTV:CAC is considered the gold standard in benchmarking SaaS companies, it has a few limitations.

First, LTV is backweighted. Churn rates are typically highest in the first few months after a cohort is acquired, meaning that by design, most of the “value” in LTV is realized late in the customer lifespan and is driven by your long tail of loyal customers.

Second, as we’ve already mentioned, LTV relies on historical data about the behavior of past customer cohorts. By optimizing against LTV:CAC, you are projecting 3-5 years into the future — and a lot can change in that time. Your product could become obsolete, driving high churn and upending your LTV assumptions.

As a result, when optimizing against LTV:CAC, you may end up waiting years to see any return on your investment — and there’s no guarantee that the return will be as great as you’d assumed. For this reason, we recommend pairing LTV:CAC with Payback Period, which measures not just the magnitude of return on acquisition spend but also the velocity of that return.

Next topic